06 Feb 2019

TP Doc Series:

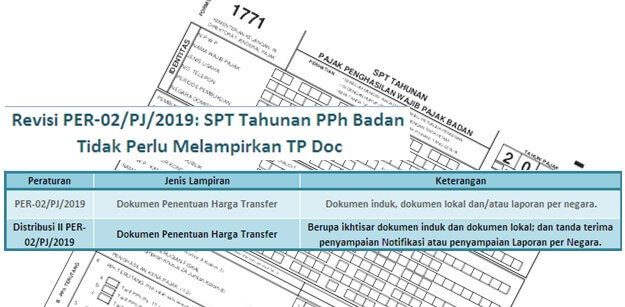

Revision PER-02 / PJ / 2019: Annual Corporate Income Tax Return Do Not Need To Attach TP Doc

Amendement of the Director General of Taxes Regulation Number PER-02 / PJ / 2019 (Distribution II) has answered the question whether the Annual Corporate Income Tax Return has to attach a Transfer Pricing Documentation (TP Doc). In connection with the previous information that the Annual Corporate Income Tax Return must attach a TP Doc (consisting of Master File, Local File and / or Country by Country Reports) in accordance with Attachment II letter J number 14 Director General of Tax Regulation Number PER-02 / PJ / 2019.

Distribution II PER-02 / PJ / 2019 confirmed that the Annual Corporate Income Tax Return is sufficient to attach an overview of the Master File and Local File and receipts of submission of Notifications or Country by Country Reports. Although they are not attached to the Annual Corporate Income Tax Return, the Director General of Taxes is still have the authority to request Master File and Local File. Thus, taxpayers are still required to provide TP Docs in accordance with the provisions stipulated in Article 4 of the Minister of Finance Regulation Number 213 / PMK.03 / 2016.

Best Regards,

ATT Consulting

Registered Tax Consultant

+62 21 2555 8567

+62 21 2555 8567

BVD Oriana User

![]()

Read Other Updates

-

Perizinan Berusaha Jasa Konstruksi (SBU dan SKK)

04 Mar 2022

-

Ketentuan Saksi-Saksi Di Dalam Hukum Perdata

25 Feb 2022

-

Hak Waris Anak Di Luar Kawin

24 Feb 2022

-

Status Hukum Harta Bawaan dan Harta Bersama Ketika Perceraian

17 Feb 2022

-

Kewajiban Melaporkan Izin Kawasan Berikat Bagi Perusahaan Yang Melakukan Perubahan Nama

02 Feb 2022

-

Penundaan Peluncuran Sistem OSS RBA oleh Kementerian Investasi

18 Jul 2021

-

Ketentuan Minimum Modal Disetor Untuk Perusahaan Penanaman Modal Asing

07 May 2021

-

Wajah Baru Online Single Submission Risk Based Approach (OSS - RBA)

02 Mar 2021