06 Feb 2019

TP Doc Series:

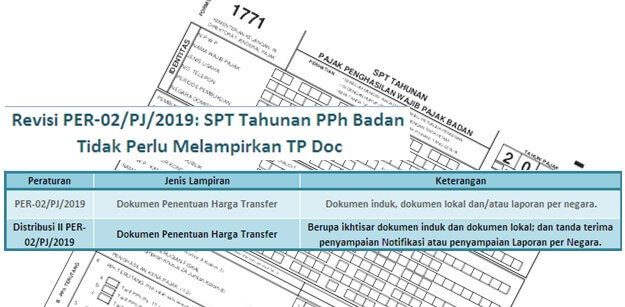

Revision PER-02 / PJ / 2019: Annual Corporate Income Tax Return Do Not Need To Attach TP Doc

Amendement of the Director General of Taxes Regulation Number PER-02 / PJ / 2019 (Distribution II) has answered the question whether the Annual Corporate Income Tax Return has to attach a Transfer Pricing Documentation (TP Doc). In connection with the previous information that the Annual Corporate Income Tax Return must attach a TP Doc (consisting of Master File, Local File and / or Country by Country Reports) in accordance with Attachment II letter J number 14 Director General of Tax Regulation Number PER-02 / PJ / 2019.

Distribution II PER-02 / PJ / 2019 confirmed that the Annual Corporate Income Tax Return is sufficient to attach an overview of the Master File and Local File and receipts of submission of Notifications or Country by Country Reports. Although they are not attached to the Annual Corporate Income Tax Return, the Director General of Taxes is still have the authority to request Master File and Local File. Thus, taxpayers are still required to provide TP Docs in accordance with the provisions stipulated in Article 4 of the Minister of Finance Regulation Number 213 / PMK.03 / 2016.

Best Regards,

ATT Consulting

Registered Tax Consultant

+62 21 2555 8567

+62 21 2555 8567

BVD Oriana User

![]()

Read Other Updates

-

Annual Year End Dinner 2023 @Satoo Shangri-La Hotel

29 Dec 2023

-

Kewajiban Perusahaan Lapor atas Data Industri dan Data Kawasan Industrinya

07 Dec 2022

-

Solusi Terbaik Restrukturisasi Perusahaan Melalui Jalur PKPU

07 Oct 2022

-

Pekerja Lain Ikut Berpartisipasi Mogok Kerja Di Perusahaan Yang Berbeda

20 May 2022

-

Kewajiban Saksi Di Pengadilan Dalam Perkara Pidana Dan Perdata

28 Apr 2022

-

Tugas Pokok, Fungsi Dan Peran Satuan Pengamanan (Satpam)

22 Apr 2022

-

Pecah Kongsi Dalam Sengketa Bisnis

06 Apr 2022

-

Kepailitan Suatu Perusahaan Yang Telah Dihomologasi Dalam Perkara Kepailitan/PKPU

15 Mar 2022