20 Jan 2017

New Tax Regulation On Transfer Pricing Issues

The Minister of Finance of the Republic of Indonesia (MoF) has issued Regulation No. 213/PMK.03/2016 and effective 30 December 2016 onward, the taxpayers who have related party transaction should prepare and maintain Transfer Pricing Documentation (TP Doc).

This regulation is issued primarily in relation to the transfer pricing documentation requirements and does not override the existing transfer pricing regulations governing the application of the arm’s length principle, i.e. Directorate General of Taxation (DGT) No. PER-43/PJ/2010 (as amended by DGT Regulation No. PER-32/PJ/2011).

By the DGT No. 32/PJ/2011 only applies for the Taxpayers who have related party transaction with foreign entity. But MoF No. 213/PMK.03/2016 was expanded applying for the Taxpayers who have related party transaction with the local and foreign entity.

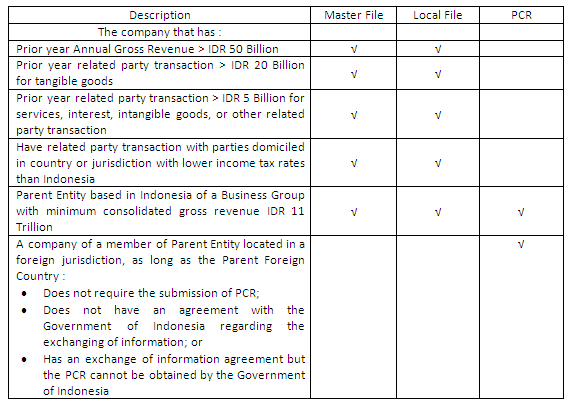

I. Type of Documents

Based on the regulation, the following documents requirements as part of TP Doc :

A. Master File

B. Local File

C. Per Country Report (PCR)

II. Requirements

The requirement for the taxpayers who have related party transaction and should prepare TP Doc, as follow :

In the event the preceding tax year covers a period less than 12 months, the gross revenue or the related party transactions are required to be annualized.

III. Timeline

The timeline for prepared and maintain the TP Doc, as follow :

- Master File and Local File must be available within 4 (four) months after the end of the tax year and must be accompanied by a statement letter concerning the time of the availability of such documents. Such statement letter is required to be submitted along with Annual Corporate Tax Return.

- The PCR must be available within 12 (twelve) months after the end of the tax year and required to be filed with the Annual Corporate Tax Return for the next year, i.e : Tax Year 2017.

IV. Language

TP Doc (Master File, Local File, and Per Country Report) should be prepared in Indonesian language. However if the Taxpayers who have an DGT’s approval to use a foreign language and currency bookkeeping could prepare TP Doc using that foreign language and accompanied with the translated Indonesian version.

If there is any further question / comments, please contact ATT Consulting at 021-25558567 or contact to :

Agung Tjahjady SH, CPA, MM, BKP (Managing Partner) - 0816 825 348

Registered Tax Consultant, Advocate

BVD Oriana User

![]()

Read Other Updates

-

Jenis Perizinan/Bidang Usaha Yang Tidak Dapat Disatukan Dengan Bidang Usaha Yang Lain (Single Purpose)

01 Mar 2019

-

Logo Perusahaan, Hak Cipta atau Hak Merek?!

22 Feb 2019

-

TP Doc Series:

06 Feb 2019

-

Polemik yang Belum Usai dari Lahirnya PMK 229/2017

31 Dec 2018

-

Kebijakan Perluasan Tax Holiday dan Pemberlakuan Mini Tax Holiday

10 Dec 2018

-

Paket Kebijakan Ekonomi XVI terhadap Investasi di Indonesia

29 Nov 2018

-

AT Thank You

01 Nov 2018

-

Perbaharui Perijinan Perusahaan Anda Jika Tidak Ingin Dibekukan

30 Oct 2018