06 Feb 2019

TP Doc Series:

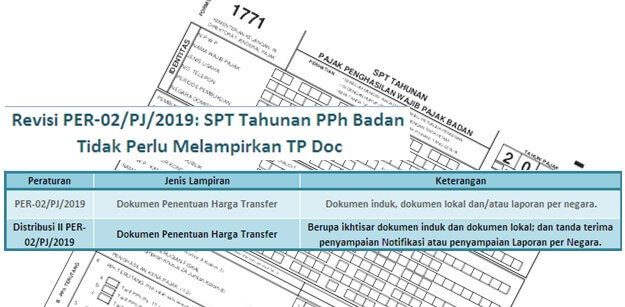

Revision PER-02 / PJ / 2019: Annual Corporate Income Tax Return Do Not Need To Attach TP Doc

Amendement of the Director General of Taxes Regulation Number PER-02 / PJ / 2019 (Distribution II) has answered the question whether the Annual Corporate Income Tax Return has to attach a Transfer Pricing Documentation (TP Doc). In connection with the previous information that the Annual Corporate Income Tax Return must attach a TP Doc (consisting of Master File, Local File and / or Country by Country Reports) in accordance with Attachment II letter J number 14 Director General of Tax Regulation Number PER-02 / PJ / 2019.

Distribution II PER-02 / PJ / 2019 confirmed that the Annual Corporate Income Tax Return is sufficient to attach an overview of the Master File and Local File and receipts of submission of Notifications or Country by Country Reports. Although they are not attached to the Annual Corporate Income Tax Return, the Director General of Taxes is still have the authority to request Master File and Local File. Thus, taxpayers are still required to provide TP Docs in accordance with the provisions stipulated in Article 4 of the Minister of Finance Regulation Number 213 / PMK.03 / 2016.

Best Regards,

ATT Consulting

Registered Tax Consultant

+62 21 2555 8567

+62 21 2555 8567

BVD Oriana User

![]()

Read Other Updates

-

Surat Tanda Pendaftaran Waralaba

25 Oct 2019

-

Pelaporan Kegiatan Lalu Lintas Devisa untuk Pinjaman Luar Negeri Swasta

18 Oct 2019

-

Audit Hukum Hak Asasi Manusia dalam Sektor Industri

04 Oct 2019

-

Outing 21-25 September 2019 @Hainan

30 Sep 2019

-

Dapatkah Mendirikan PT Dengan Bentuk Penyetoran Inbreng?

27 Sep 2019

-

Persiapan Pendirian PT PMA Setelah Lahirnya OSS versi 1.1

20 Sep 2019

-

Kepastian Hukum Dalam Peralihan Kepemilikan Tanah dan Bangunan Pada Dunia Bisnis Dan Investasi Properti

13 Sep 2019

-

Mengenal e-Court/ Persidangan Secara Elektronik

06 Sep 2019